The primary objective of CCAR secured model is to stress test the business unit’s mortgage balances using a set of scenarios provided by the Federal Reserve Bank (FRB) as well as Bank Holding Company’s (BHC). Therefore, a critical step in the model development is to identify statistically significant relationships between loan performance and a set of macroeconomic variables. Establishing these relationships allows the model development team to construct a method for producing projections of mortgage performance under periods of market stress.

The primary objective of CCAR secured model is to stress test the business unit’s mortgage balances using a set of scenarios provided by the Federal Reserve Bank (FRB) as well as Bank Holding Company’s (BHC). Therefore, a critical step in the model development is to identify statistically significant relationships between loan performance and a set of macroeconomic variables. Establishing these relationships allows the model development team to construct a method for producing projections of mortgage performance under periods of market stress.

Intended Use of the Model

This model is used to estimate PD (180+ DPD – units at portfolio level) for mortgage portfolio through ARIMAX methodology. The model forecasts credit losses in support of capital planning and regulatory mandated stress testing. The model is used to forecast losses for the CCAR macroeconomic scenarios (baseline and adverse).

Modelling Process

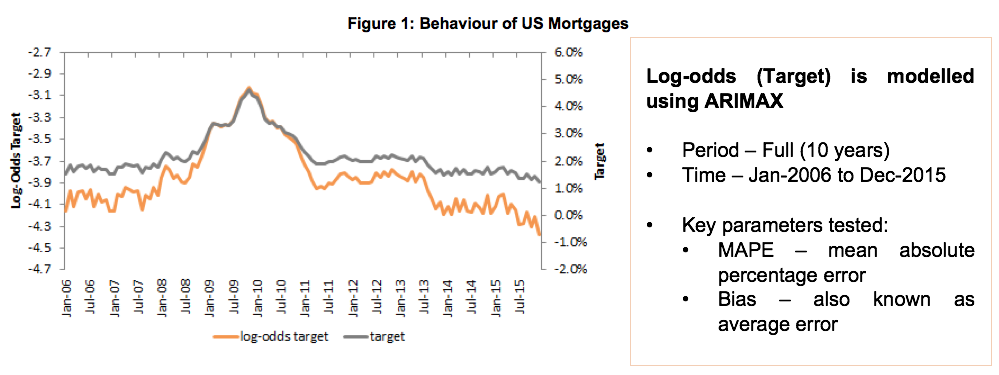

The portfolio level data is provided for model development. The dependent variable chosen for this study is the log-odds of the probability of an account to go into 180+ DPD in a particular month for US Mortgages.

Equation 1: Log Odds (Target)

| Log-odds (Target) = LN (Def Rate / (1 – Def Rate)) |

The graph below shows the behaviour of US Mortgages over 10 years. The candidate macroeconomic variables are US unemployment, US GDP, US HPI, US CPI, Oil prices, US / EUR exchange rate, and Fed Rates. Each variable is available along with the scenarios associated with the level of stress mentioned previously.

Co-integration

Co-integration in the simple case of 2 time series x(t) and y(t) that are both integrated of order one i.e. I(1), then x(t) and y(t) are said to be co-integrated if there exists a parameter “r” such that u(t) = y(t) – r * x(t) is a stationary process. In general, regression models for non-stationary variables gives spurious results. Only exception is if the model eliminates the stochastic trends to produce stationary residuals.

If x(t) and y(t) are co-integrated then u(t) is white noise. If x(t) and y(t) do not co-integrate then u(t) is not white noise and the deviation of u(t) is I(1).

Modelling Outcome

There are several main model assumptions which include stationarity of residuals, no serial autocorrelation in residuals, statistical significance associated with exogenous variables, no multi-collinearity among independent variables and exogenous variables should exhibit correct sign. The stationarity of residuals and no serial autocorrelation in residuals are discussed below:

Back Testing

The objective of this section is to evaluate the performance of the model by comparing the accuracy of the model over the forecasted horizon. The current application of the model is for use in forecasting stress losses for CCAR, which has a 27-months forecast horizon.

Back Testing Design

Table 3: Back Testing

| Back Testing | Period | Time |

| BT 1 | Recent | Oct-2013 to Dec-2015 |

| BT 2 | Stress | Jul-2008 to Sep-2010 |

Back Testing Results

Model Accuracy

Accurate prediction of future default rates is a major concern for both the Bank Holding Company (BHC) and Federal Reserve Bank (FRB). The macroeconomic factors (Unemployment, GDP, CPI, HPI, etc.) are key derivers of the default rates. The results of model accuracy are discussed below:

Table 4: Model Robustness (MAPE and Bias) *

| Period | Time | MAPE | Bias | |

| Model | Full | Jan-2006 to Dec-2015 | 5.75% | -0.22% |

| Back Testing 1 | Recent | Oct-2013 to Dec-2015 | 9.31% | -4.20% |

| Back Testing 2 | Stress | Jul-2008 to Sep-2010 | 6.19% | 2.76% |

*Note: The time frame for Back Testing 1 and Back Testing 2 is 27 months

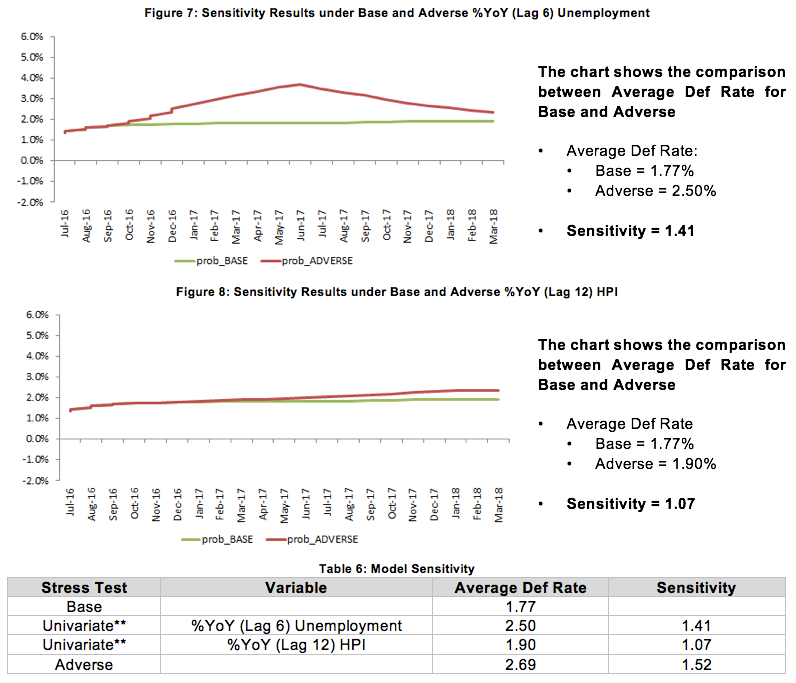

Model Sensitivity

The approach taken to test sensitivity is to run the BHC stress test scenarios to the last monthly observation in the dataset. The forecast starts from Jan-2016 and runs 27 months through Dec-2018. The forecast has base and adverse scenarios.

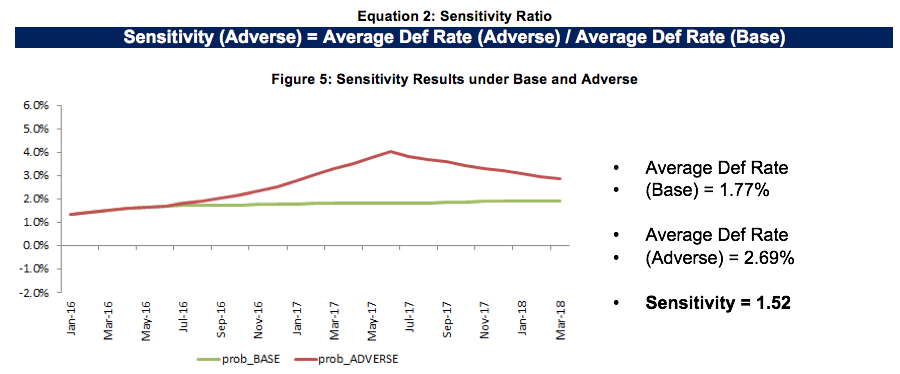

Sensitivity of Model Results under Base vs Adverse Macro Scenarios

To measure the sensitivity of the model, default rate was forecasted for Base Scenario and Adverse Scenario. As observed from the results, the model is very sensitive to macro-economic changes. The divergence in forecast for base and adverse has not started until 6-9 months after snapshot. The adverse scenario forecast is 1.5 times higher than base scenario.

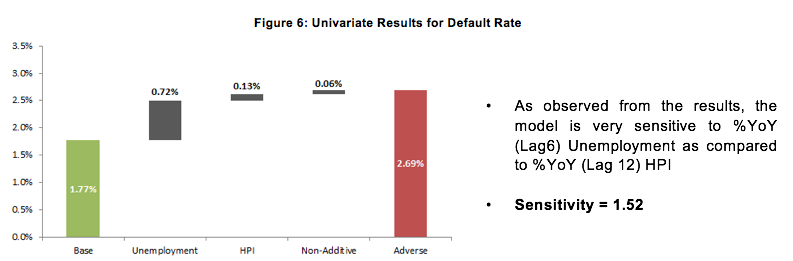

Sensitivity of Model Results to Changes in Underlying Macro Variables

To measure the sensitivity of the underlying macro variables, default rate was forecasted for Base Scenario and one macro variable was stressed at a time.

**Note: To measure the sensitivity of the underlying macro variables, default rate was forecasted for Base Scenario and one macro variable was stressed at a time.

Conclusion

A central goal of the capital plan rule is to ensure that BHCs have robust internal practices and policies to determine the appropriate amount and composition of their capital, given the BHC’s risk exposure and corporate strategies. The main goal of this exercise is to arrive with most reliable and robust process of translating stress in economy to stress in balance sheet of BHCs. The model should be sensitive enough so that clear separation of scenarios is presented.

The following result allows assessing bank’s position in mortgages during stress. There is a clear separation of base and adverse scenario.